Provided to subscribers October 18th.

Here is the latest from Canadian Value Investors!

Solitron SODI /Ammo, Inc. POWW Updates

Petrobras – Highest production ever

Investing in Japan

Ideas from around the world - Investing in Bhutan

China Tensions

We would first like to say that we do not mean to be doomsayers, even though our portfolio being weighted towards guns, oil, and canned vegetables might give this appearance. They are just the best opportunities we have found at the moment and, oddly enough, the original purchases were not driven by the macro tailwinds we are having. We are actively seeking out happier ideas. If only the LEGO Group was a public company. https://www.lego.com/en-us/aboutus/lego-group

Solitron SODI /Ammo, Inc. POWW Updates

Disclosure: We continue to own these.

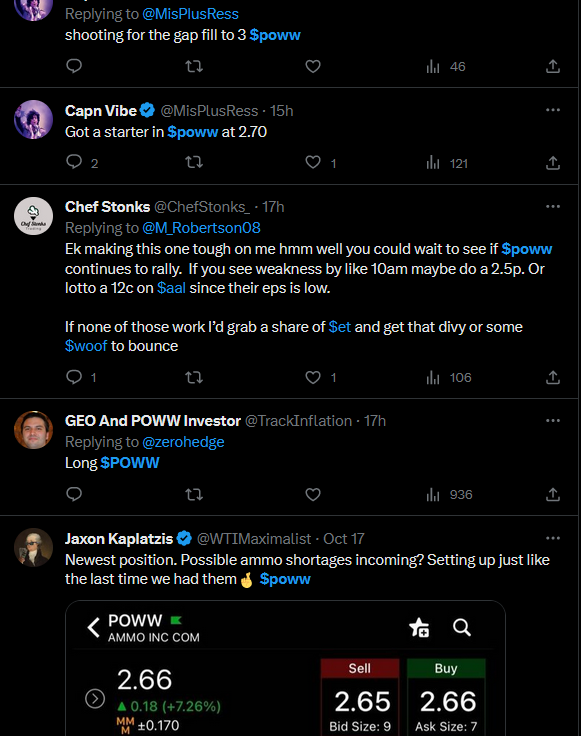

Since our last update, Hamas attacked Israel and concerns it might turn into a much larger issue has brought even more attention to defence/gun companies. Here is a chart of our two related holdings as well as some large cap peers that we do not own. Ammo appears to be outrunning the rest on no news. There does seem to be an uptick in garbage posts on Twitter about it (see next), which might be playing a role given the small market cap (previously ~$200MM, now ~$300MM).

Solitron provided a bit more color on their acquisition of Micro Engineering. We also found the actual stock purchase agreement via a filing. Here you go. https://www.sec.gov/Archives/edgar/data/91668/000165495423011547/sodi_ex101.htm

Effective September 1 Solitron closed its acquisition of Micro Engineering Inc. (MEI) based in Apopka, Florida. MEI specializes in solving design layout and manufacturing challenges while maximizing efficiency and keeping flexibility to meet unique customer needs. Since 1980 the MEI team has been dedicated to overcoming obstacles to provide cost efficient and rapid results. MEI specializes in low to mid volume projects that require engineering dedication, quality systems and efficient manufacturing.

The transaction was structured as a stock purchase. An initial payment of $3.0 million was made at closing. Additional earnout payments of up to 7.5% of annual revenue, or approximately $450,000 each, would be payable over each of the next three years. MEI produces electronic components primarily for the medical industry. Revenue for 2022 was approximately $5.9 million (unaudited) as compared to approximately $5.5 million (unaudited) in 2021. Unaudited operating income was approximately $1.3 million in 2022 and approximately $1.2 million in 2021. One customer accounted for approximately 90% of revenues in both 2021 and 2022.

The full stock purchase agreement includes full balance sheet for the working capital adjustment calculations. The table below is from the end of the report; it appears that YTD net income is running below 2021/2022, but maybe the business has some seasonality to it.

Now that the new facility is up and running, things seem to be trending in the right direction for the core business.

Net Sales. Net sales for the three months ended August 31, 2023 increased 18% to $2,579,000 as compared to $2,187,000 for the three months ended August 31, 2022. The increase in net sales was largely due to customer delivery schedules.

Net bookings for the three months ended August 31, 2023 increased 39% to $2,231,000 versus $1,607,000 during the three months ended August 31, 2022. Backlog as of August 31, 2023 increased 85% to $8,785,000 as compared to a backlog of $4,755,000 as of August 31, 2022.

Petrobras – Highest production ever

Disclosure: We continue to own this.

The good news keeps coming for Petrobras. They recently beat their all-time high production while oil floats in the $80s.

Rio de Janeiro, October 16, 2023 - Petróleo Brasileiro S.A. – Petrobras informs that it broke its quarterly record for operated oil and gas production in the third quarter of this year, with 3.98 MMboed (million barrels of oil equivalent per day), 7.8% above the second quarter. It also achieved a monthly record for operated production in September, with a volume of 4.1 MMboed, 6.8% higher than in August.

Although the stock is up 70-80% year-to-date (depending on share series and currency), it has not really moved that much… now has it? Looking back to this day in 2019, Petrobras traded at around the same market cap and an EV / earnings multiple of ~18x, while today it is trading at EV / earnings of ~5x even though oil prices are more robust, debt is well managed, and actual operating performance is stronger. But maybe shares in this business really are just worth 3-ish times earnings. We will ponder this question while we continue to collect our dividends (about 20% YTD).

Investing in Japan

Disclosure: We have no positions except through Berkshire itself.

Back in the middle of COVID, Warren Buffett bought five of the big trading houses in Japan. And in typical Buffett fashion, he has done fabulously well.

ITOCHU Corporation TSE:8001

Marubeni Corporation TSE:8002

Mitsubishi Corporation TSE:8058

Mitsui & Co., Ltd. TSE:8031

Naito & Co., Ltd. TSE:7624

Interestingly, he has recently been adding to his positions. Maybe the party is not over with P/Es of around 10x currently. Why did he invest in the first place? Here’s an overview we found.

Value Punks' Daye Deng on why Warren Buffett $BRK invested in Japanese Trading Companies https://podcasts.apple.com/ca/podcast/yet-another-value-podcast/id1526149547?i=1000631149927

If the large caps are interesting, might not the microcaps be even more interesting? Some think so. We ourselves are interested, but we would be starting from scratch and are finding wonderful opportunities locally. Still, maybe we should look closer.

The Case for Japanese MicroCaps with David Baeckelandt, Head of Client Relations at SuMi TRUST https://podcasts.apple.com/ca/podcast/planet-microcap-podcast-microcap-investing-strategies/id1024217659?i=1000631057120

Ideas from around the world - Investing in Bhutan

Disclosure: We have no investments in Bhutan.

The Royal Securities Exchange of Bhutan (RSEB) is one of the smallest in the world with a total market capitalization of its listed companies totaling ~$700M at the time of this writing. The exchange opened in 1993 and offered electronic trading in 2012. There are currently 19 companies listed on the exchange.

https://opusletter.substack.com/p/investing-adventures-in-bhutan

China Tensions - First case of expropriation of Chinese assets in the U.S.?

Arkansas has become the first state to order that a Chinese company give up ownership of local land, amid fears of attempts by Beijing to malignly infiltrate and influence the U.S. through various means.

On Tuesday, Governor Sarah Huckabee Sanders announced that she was ordering Syngenta to relinquish its 160 acres of land holdings in northeastern Arkansas, accusing its owner of "posing a clear threat to our state." The Switzerland-headquartered agricultural chemicals producer was acquired in 2017 by the state-owned China National Chemical Corporation, and primarily trades in pesticides and seeds.

https://www.newsweek.com/china-land-arkansas-sarah-huckabee-sanders-1835652