Reflecting on 2025, Navigating 2026, Colabor vs Canlan

Always Think About Liquidity – Spreads Low, Risks High

Here is the latest from Canadian Value Investors!

Reflecting on 2025

Nathan’s Hot Dogs Were On Sale

Thinking About Relative Value with Thinkific TSX:THNC

Navigating 2026 – A Sign of the Times

Always Think About Liquidity – Spreads Low, Risks High

Colabor Complacency – A Quick Case Study

Canlan Sports TSX:ICE – Keeping it simple

Reflecting on 2025

We would first like to thank all of you for your ongoing support! Last year was busy here at Canadian Value Investors:

We covered conferences, including Cheatsheets for Planet MicroCap and SmallCap Discoveries covering every company.

We did deep dives of names like Velan Inc., D-Box, Goldmoney, Canlan Sports, and Gamehost. We keep a directory here - https://www.canadianvalueinvestors.com/directory

We dipped our toes into new industries like cannabis, with overviews of Rubicon and Cannara (we remain long both). Our first post here - https://www.canadianvalueinvestors.com/p/the-curious-case-of-canadian-cannabis

We look forward to doing even more in 2026!

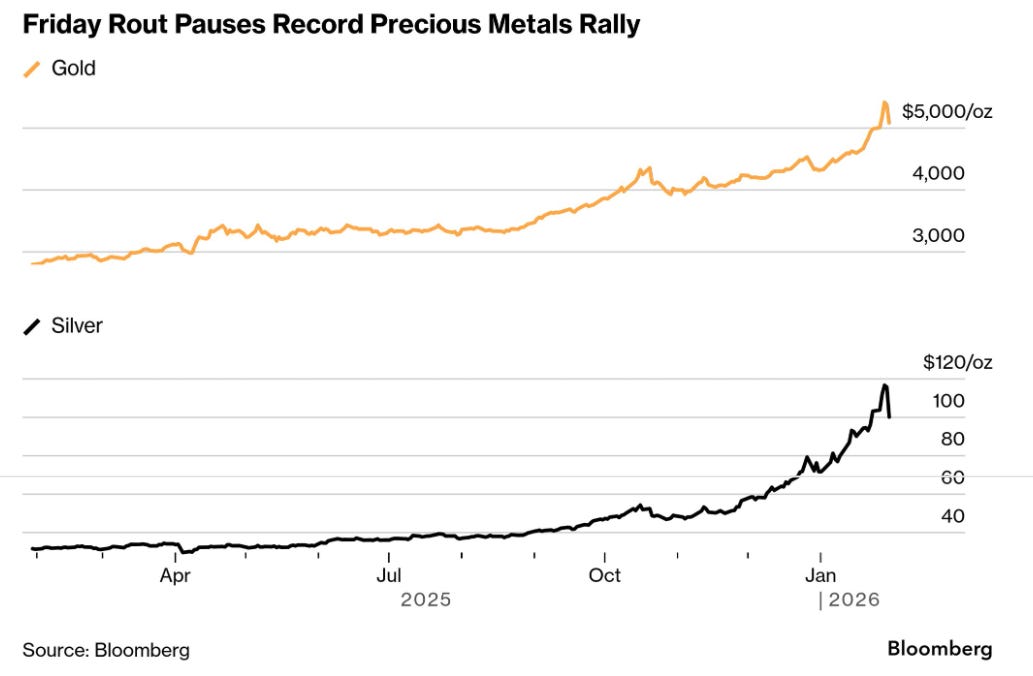

We spent more time than usual this January reflecting on the past year. In part, it was because of how odd the year was. Our portfolios did well, exceeding the typical benchmarks, but we could have also just bought a few gold bars and gone to the beach.

Our favourite investing and general life paradox: If you didn’t make the mistakes you have made so far, including the terrible ones, would you have been able to get as far as where you are? With the benefit of hindsight, we now have a long list of missed investments, a few terrible ones, and a laundry list of life decisions we could have made better. But the irony is that if we didn’t miss that first investment or make that first big mistake, maybe we wouldn’t have made it at all.

And what do you do about all of this? Just keep going.

Disclaimer - The content contained in this blog represents the opinions of contributors. You should assume contributors have positions in the securities discussed, whether long, short, or somewhere in between, and that this creates an obvious bias and conflict of interest regarding the objectivity of this blog. Statements in the blog are not guarantees of future performance whatsoever and are subject to certain risks, uncertain risks, and other factors. Information might also be completely out of date and may or may not be updated. In addition, no one guarantees the accuracy of any information provided and none of the information should be construed as investment advice or any other kind of advice under any circumstance, and the blog is a blog and not a registered investment advisor or broker in any jurisdiction. Frankly, no information here should be used for any purpose, except for entertainment (and we hope you enjoy).

Nathan’s Hot Dogs Were on Sale

As we wrote last March:

Nathan’s Famous hot dogs started in 1916 and is now the most famous hot dog in the world. It has been steadily growing brand value and cash flows, primarily through its licensing and branded products, while de-levering their balance sheet. It also happens to have a key owner that we think wants to sell and a newly public key partner [Smithfield Foods] looking for stable cash flows that can afford to buy. A 25-50% offer above the current share price would not be unreasonable and appears like it could happen soon.

The strategic partner did indeed buy them out. It was just announced and a reasonable outcome for shareholders, albeit below summer speculative highs.

SMITHFIELD, Va., January 21, 2026 / -- Smithfield Foods, Inc. (Nasdaq: SFD) (“Smithfield Foods” or “Smithfield”), an American food company and an industry leader in value-added packaged meats and fresh pork, and Nathan’s Famous, Inc. (Nasdaq: NATH) (“Nathan’s Famous”), today announced that they have entered into a definitive merger agreement for Smithfield Foods to acquire all of Nathan’s Famous’ issued and outstanding shares for $102.00 per share in cash, which represents an enterprise value of approximately $450 million… The transaction represents a valuation of approximately 12.4x Nathan’s Famous’s LTM adjusted EBITDA2 and a multiple of approximately 10.0x post- synergies. Smithfield Foods expects to achieve annual cost synergies of approximately $9 million by the second anniversary of the deal closing

Thinking About Relative Value with Thinkific TSX:THNC

As we covered in Fallen Darlings in November, we think the set up of Thinkific today is interesting and we remain long. It is also a good case study. AI has created widespread concern in various tech names, including Constellation and Duolingo (no positions, evaluating).

We always keep in mind expectations and value. Duolingo reported Q3 revenue growth of 41% in to ~$270MM, a 36% increase in users to 50+ million, and yet there was a 8% decline in the stock price at time of writing.

In Thinkific’s case, if they were to drop another 50% they would be trading roughly for the cash on hand and no debt, with the business (that is making interesting changes) for free. This is not a stock with high expectations built in, which we always like. We also think management knows something needs to be done this year and will do their best to make changes accordingly.

https://www.canadianvalueinvestors.com/t/thnc

Navigating 2026 – A Sign of the Times

We have to say this is an interesting investing environment. Fears of an AI bubble, precious and base metals taking off, and a calm loose lending market in the background. This might understandably leave a value investor scratching their head.

To help keep us grounded, we go back to one of our favourite investors, Stanley Druckenmiller of Quantum Fund fame and formerly lead portfolio manager for George Soros. He has had a remarkably successful investing career, with many great big bets. But he also made the worst mistake ever in 2000, buying at the peak of the Dotcom boom.

I made a lot of mistakes, but I made one real doozy. So, this is kind of a funny story, at least it is 15 years later because the pain has subsided a little. But in 1999 after Yahoo and America Online had already gone up like tenfold, I got the bright idea at Soros to short internet stocks. And I put 200 million in them in about February and by mid-March the 200 million short I had, lost $600 million on, gotten completely beat up and was down like 15 percent on the year. And I was very proud of the fact that I never had a down year, and I thought well, I’m finished.

So, the next thing that happens is I can’t remember whether I went to Silicon Valley or I talked to some 22-year-old with Asperger’s. But whoever it was, they convinced me about this new tech boom that was going to take place. So I went and hired a couple of gunslingers because we only knew about IBM and Hewlett-Packard. I needed Veritas and Verisign. I wanted the six. So, we hired this guy and we end up on the year — we had been down 15 and we ended up like 35 percent on the year. And the Nasdaq’s gone up 400 percent.

So, I’ll never forget it. January of 2000 I go into Soros’s office and I say I’m selling all the tech stocks, selling everything. This is crazy…at 104 times earnings. This is nuts. Just kind of as I explained earlier, we’re going to step aside, wait for the next fat pitch. I didn’t fire the two gunslingers. They didn’t have enough money to really hurt the fund, but they started making 3 percent a day and I’m out. It is driving me nuts. I mean their little account is like up 50 percent on the year. I think Quantum was up seven. It’s just sitting there.

So like around March I could feel it coming. I just — I had to play. I couldn’t help myself. And three times the same week I pick up a — don’t do it. Don’t do it. Anyway, I pick up the phone finally. I think I missed the top by an hour. I bought $6 billion worth of tech stocks, and in six weeks I had left Soros and I had lost $3 billion in that one play. You asked me what I learned. I didn’t learn anything. I already knew that I wasn’t supposed to do that. I was just an emotional basket case and couldn’t help myself. So, maybe I learned not to do it again, but I already knew that.

Another lesson from Stanley is to always think about market liquidity.

Always Think About Liquidity – Spreads Low, Risk High

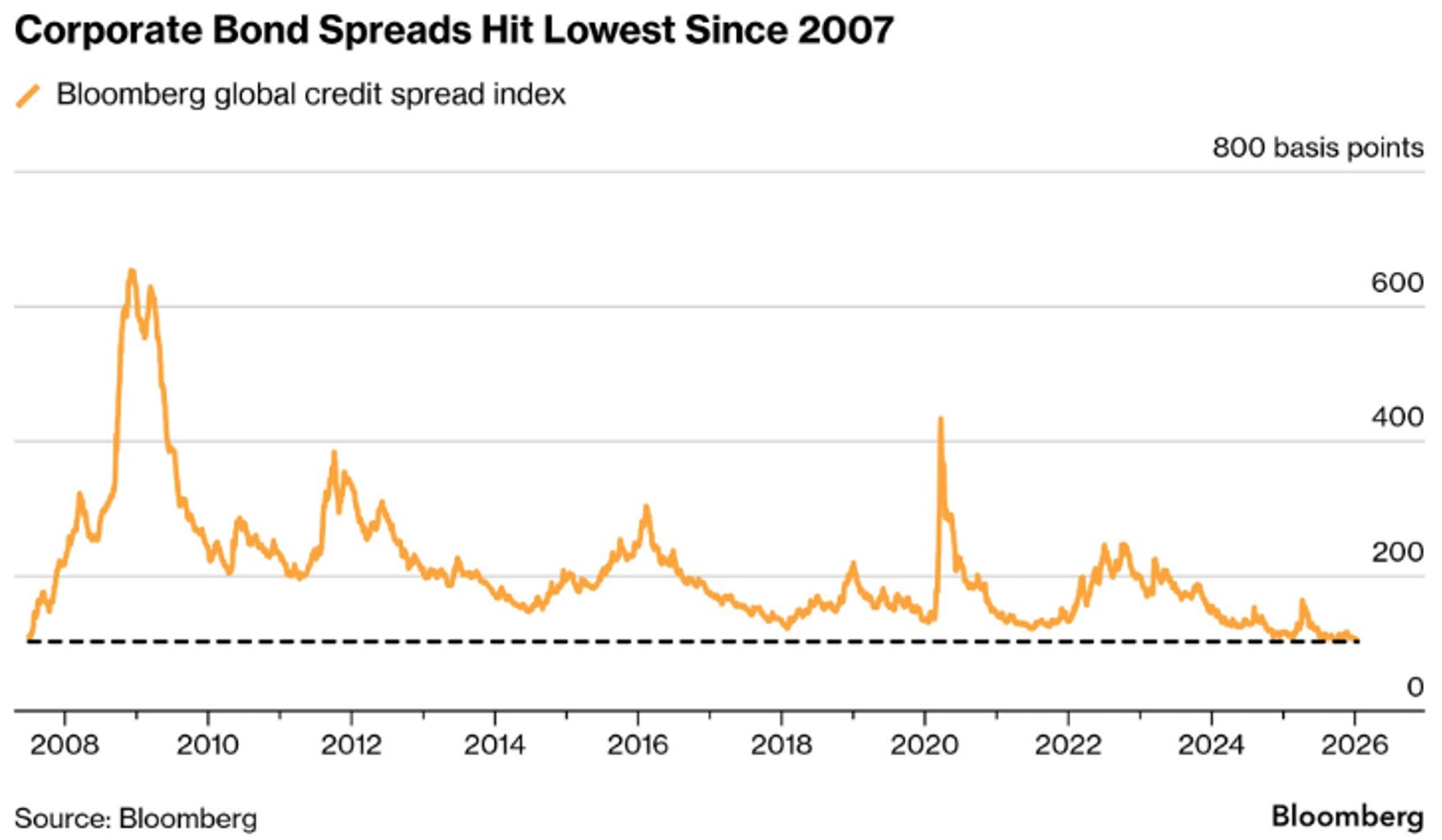

We fret. There is lots of talk about inflated valuations and sticky inflation, both which we worry about. However, another concern we have that is less talked about is the complacency of the debt market. It appears the lenders of the world are reading different newspapers than we are, and that means if there is any sort of hiccup, the reversal could be quite sharp. We view the following case as a canary.

For now, many money managers continue to dive into the rally, in part due to the prospect of interest-rate cuts by the Federal Reserve and other central banks. Easing could help the global economy navigate threats from President Donald Trump’s tariffs.

There’s huge demand for debt, even the riskiest sort, as investors hunt for yield. That’s being met by record supply.

The extra yield investors demand to hold junk notes is also at the lowest in almost two decades. On Monday, the US leveraged loan market had its busiest day since July, with some $35 billion of deals launched.

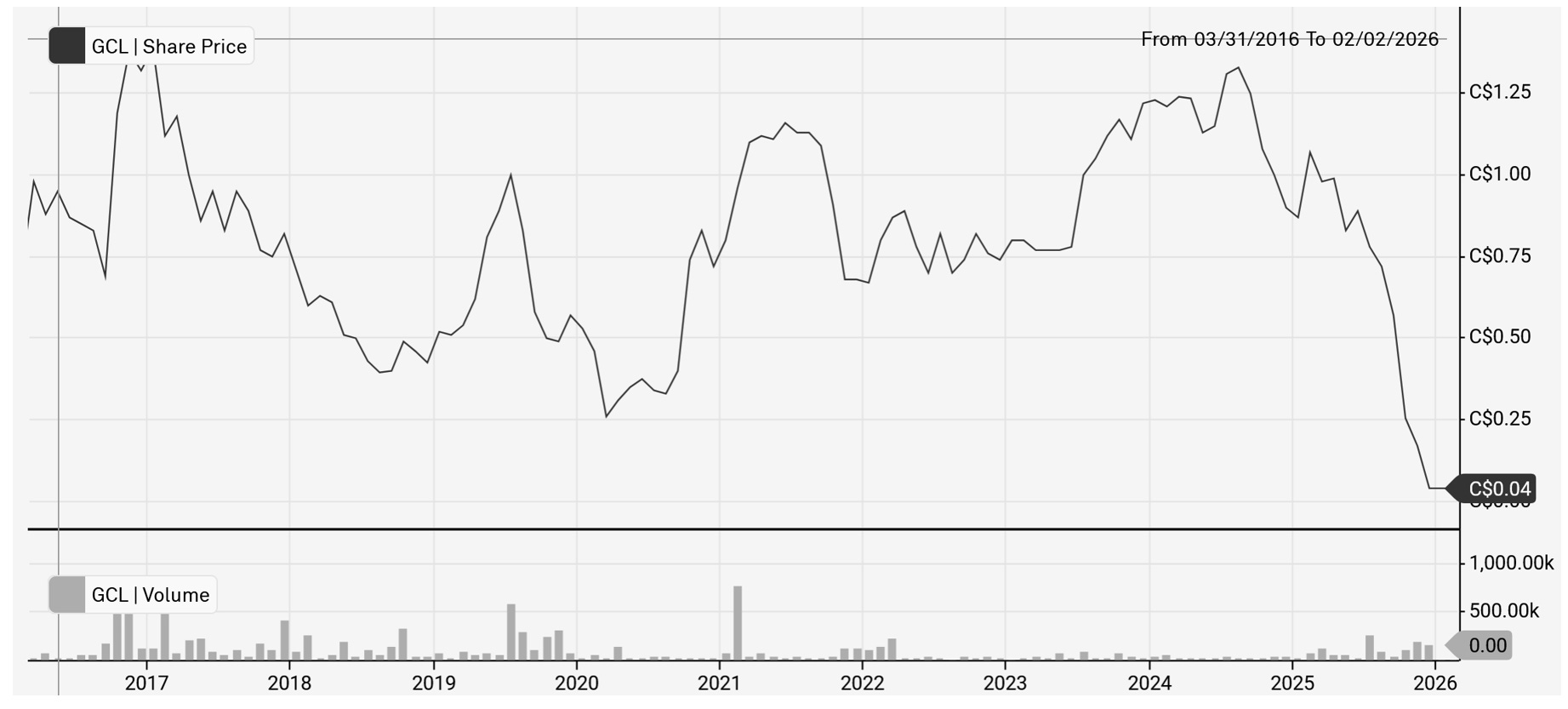

Colabor Group (TSX: GCL) Complacency – A Case Study

A great case study is Colabor Group (no position ever), which is going through a restructuring. They are a sleepy TSX name that distributes more than 10,000 food and related products from over 600 suppliers to over 5,000 customers. A pretty simple business that is typically not very exciting, but at least not often exposed to dramatic failures. Yet, here we are.