Atlas Engineered Products TSXV:AEP – Catching the bottom, Charlie Brown?

But first, an update on canned vegetables and buses

Is Atlas Engineered Products at the bottom? Possibly! But first, an update on canned vegetables and buses.

Two of our holds have done well, but have started to reach the point where we do not view them as “cheap” anymore, or at least not cheap relative to our other opportunities. We have taken two different approaches with them.

Today’s update:

-Seneca Foods (SENEA)

-NFI Group Inc. (TSX:NFI) – An exciting bumpy ride up the mountain road

-Atlas Engineered Products (TSXV:AEP) – Catching the bottom, Charlie Brown?

Disclaimer - The content contained in this blog represents the opinions of contributors. You should assume contributors have positions in the securities discussed, whether long, short, or somewhere in between, and that this creates an obvious bias and conflict of interest regarding the objectivity of this blog. Statements in the blog are not guarantees of future performance whatsoever and are subject to certain risks, uncertain risks, and other factors. Information might also be completely out of date and may or may not be updated. In addition, no one guarantees the accuracy of any information provided and none of the information should be construed as investment advice or any other kind of advice under any circumstance, and the blog is a blog and not a registered investment advisor or broker in any jurisdiction. Frankly, no information here should be used for any purpose, except for entertainment (and we hope you enjoy).

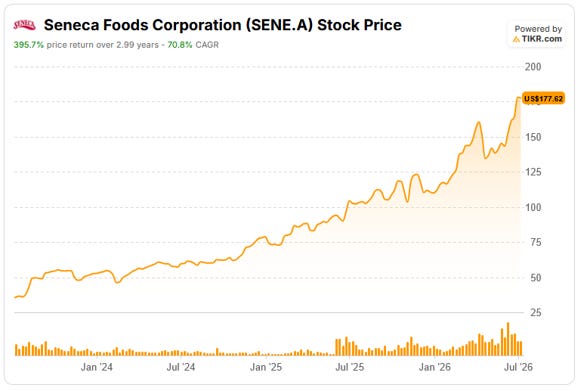

Seneca Foods (SENEA)

Who knew canned vegetables would be so exciting? We have been part of this ride since our first article in 2023. The underlying business has actually performed better than we expected, but the stock has even more so to the point that we have significantly reduced our holdings.

Full archives: https://www.canadianvalueinvestors.com/t/senea

A major development over the past year for our industry, as well as for the Company, was the bankruptcy of Del Monte Foods. Their unsustainable debt along with other factors led to the filing in July 2025, kicking off a prolonged, court-supervised auction process that did not reach its conclusion until mid-March 2026. The business was ultimately split up into three parts with the new owners of the vegetable business assuming the Supply Agreement that we have had with the bankrupt entity since 2019, and which was revised in 2023. We look forward to continuing to supply a major portion of the needs of the Del Monte brand to the new owners and look forward to solidifying a long and mutually beneficial relationship with them.

…

Our acquisition of the Green Giant Shelf-stable business in November 2023 has been fully stabilized and integrated with our other shelf-stable businesses. However, the fate of the Green Giant Frozen business in the U.S and the associated IP, had remained in limbo. We were extremely pleased to be able to come to an agreement with the previous Green Giant Frozen owner to subsequently acquire that business…This acquisition more than doubles the size of our frozen business and not only helps diversify our portfolio but makes us a legitimate player in the frozen channel. We feel that this positions us well for both organic growth as well as acquisition opportunities that might develop. We are very pleased with where we are with Green Giant.

…

[Note LIFO accounting continues to create noise we suggest you adjust for] The Company recorded a LIFO credit of $22.3 million in fiscal year 2026 versus a LIFO charge of $34.5 million in fiscal year 2025, which equated to a year-over-year favorable impact to gross margin of $56.8 million. [FY 2026 operating income was $148MM]

NFI Group Inc. (TSX:NFI) – An exciting bumpy ride up the mountain road

It appears the market is starting to recognize the NFI turnaround. The battery hiccup last fall did turn out to be a great buying opportunity. Again, things have moved faster than we thought they would. It is not quite too expensive, but not cheap enough to buy. So, we are being a bit more creative here. We have sold some end-of-year OTM calls with a strike price at around ~$30, providing a ~9% annualized “dividend” based on today’s price while we continue to benefit from ongoing improvements in the business and avoid capital gains tax. If NFI gets too far ahead of its underlying improvements and hits $30 before year-end (an EV/market cap far beyond the catching-up-cashflow), a 25%+ return from today, we are just fine with getting off the bus.

Full archives: https://www.canadianvalueinvestors.com/t/nfi

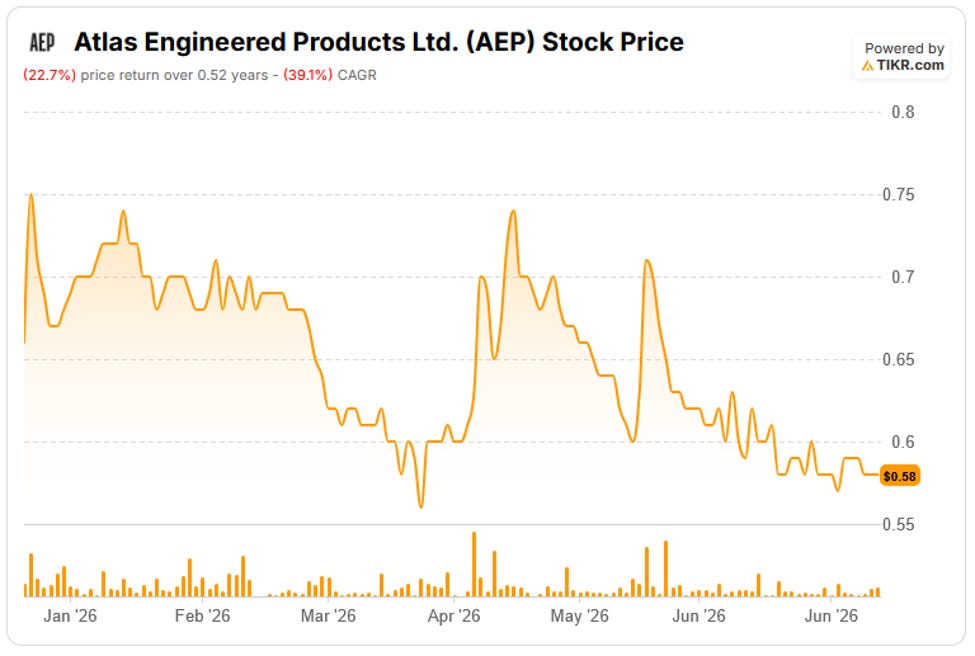

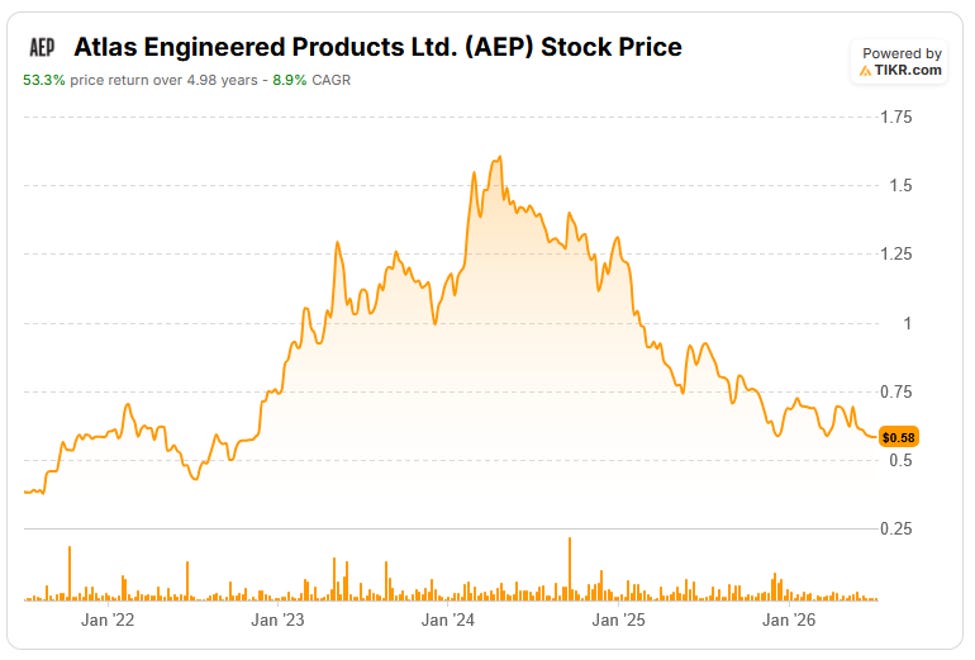

Atlas Engineered Products TSXV:AEP – Catching the bottom, Charlie Brown?

We first wrote about Atlas last January – “Atlas Engineered Products TSXV:AEP – Framing the future. Will consolidation and automation pay off?”

With today’s headline we are just being dramatic; we did not expect much to happen in the first two quarters, and still view this as a 2027/28 story. However, a few interesting things have happened since and thought it was worth revisiting. Their first automated plant is getting close to operating and received some government support, while the stock remains unsupported.

Clinton Ramp Up

Clinton is close. Our understanding is the building envelope is complete and now equipment is being installed with start up being late summer.

Since our last update, the Government of Canada announced $4MM of support for Atlas for this facility under Investments in Forest Industry Transformation (IFIT) Program, “for a project that will strengthen the wood construction supply chain and expand Canada’s capacity to produce high value, made-in-Canada building materials.” For context, at time of announcement this was equal to approximately 10% of Atlas’ market cap.

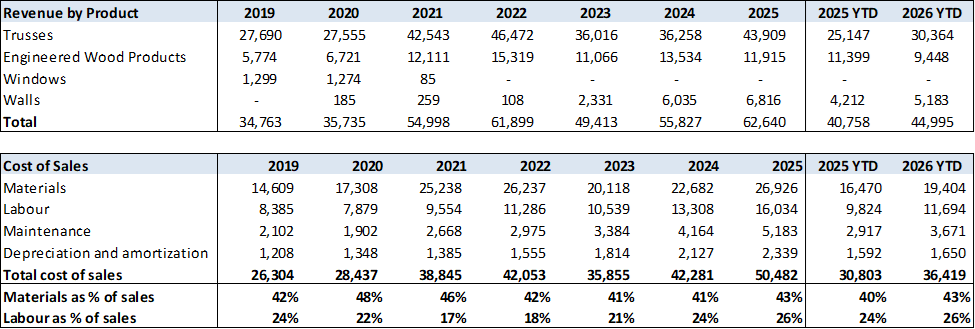

Our estimate of capacity is $15-20MM and labour cost savings could be significant (up to 50%, though we are more conservative) while most competitors cannot afford to automate. Given labour costs are ~25% of COGS, this is material. This should allow Atlas to bid on projects that were previously low margin/uneconomic (e.g. far away, large housing development with very competitive bidding) while benefiting from some incremental margin on typical projects; i.e. we expect the impact to be a blend of higher revenue and higher margin and not just straight margin increase.

What are “normal” margins anyway?