Vitreous Glass TSX:VCI Update: A case study of key contracts, compensation, and leveraged buyouts

Disclosure: We own Vitreous, albeit a small weighting, and have a soft spot for this business.

Oh Vitreous Glass, our favourite little TSX Venture nanocap. We first came across it in 2013 and first wrote it up in 2015. It is a great business case for keeping things simple. Shareholders have done well (IRR in the teens).

Today we are using it as a case study of key contracts, compensation, and what leverage can do.

Disclaimer - The content contained in this blog represents the opinions of contributors. You should assume contributors have positions in the securities discussed, whether long, short, or somewhere in between, and that this creates an obvious conflict of interest regarding the objectivity of this blog. Statements in the blog are not guarantees of future performance whatsoever and are subject to certain risks, uncertain risks, and other factors. Information might also be completely out of date and may or may not be updated. No one guarantees the accuracy of any information provided and none of the information should be construed as investment advice under any circumstance, and the blog is a blog and not a registered investment advisor or broker in any jurisdiction. Frankly, no information here should be used for any purpose except for entertainment (and we hope you enjoy).

As a recap, they crush waste glass into cullet, which is then sold to local fibreglass manufacturers (total customers: 3). The waste glass is primarily from the Alberta Recycling Management Authority, being glass container bottles, under a long-term contract they have been able to renew continually. When they started, the alternative use for the Alberta government was sending it to a landfill.

Vitreous’ customers use the cullet as it is clean and requires less energy to turn into fibreglass than raw sand. They are also supply constrained. For our overview of Vitreous, see here -

Supply constrained, or hidden opportunities?

Historically, Vitreous has been able to renew their contract with the Alberta government.

During fiscal year 2024, the Company increased the certainty of accessing raw material recycled glass with the execution of a long-term supply agreement with its main supplier. The supply agreement covers all deposit-system beverage container glass collected in Alberta and is a source of low-cost raw materials.

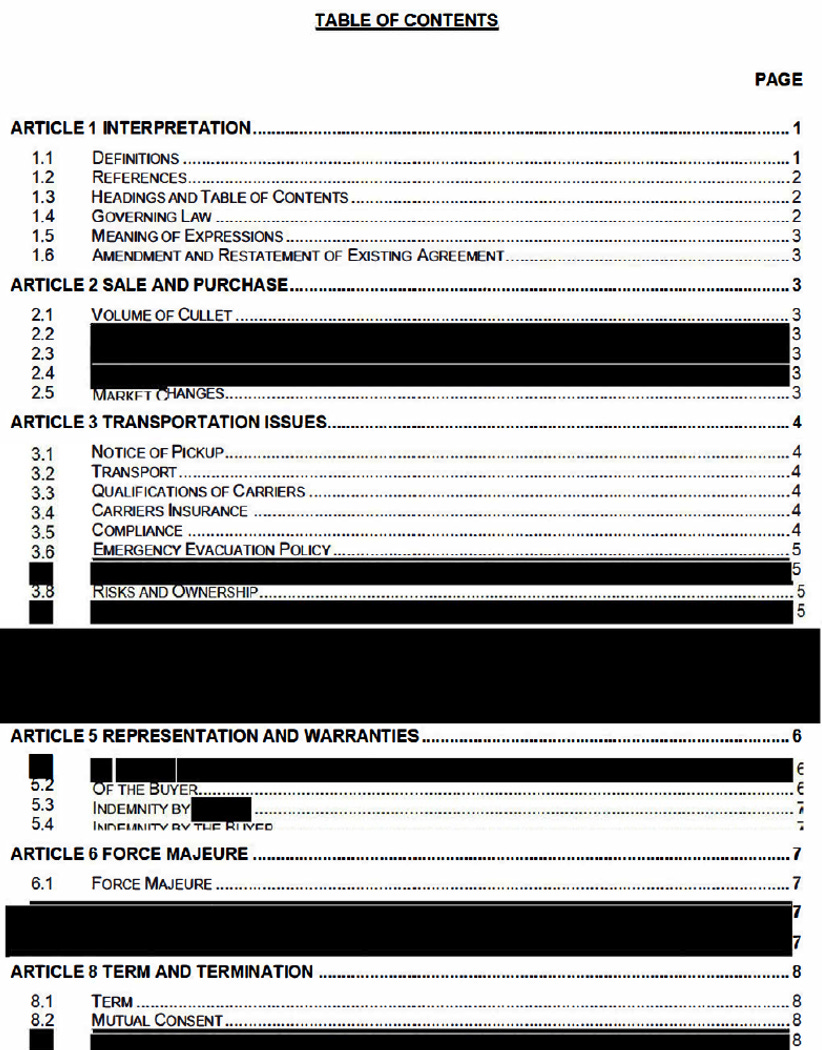

The renewed agreement is actually on SEDAR but heavily redacted.

However, the issue is that beverage containers using glass has been in structural decline (Snapple switching from glass was a big deal), partly offset by Alberta’s growing population. And Vitreous has not had much success finding other supplies, but have at least been able to put through price increases (4% 2024, 8% at end of FY2025). We assumed that no other waste glass sources of scale could be found, but they finally did.

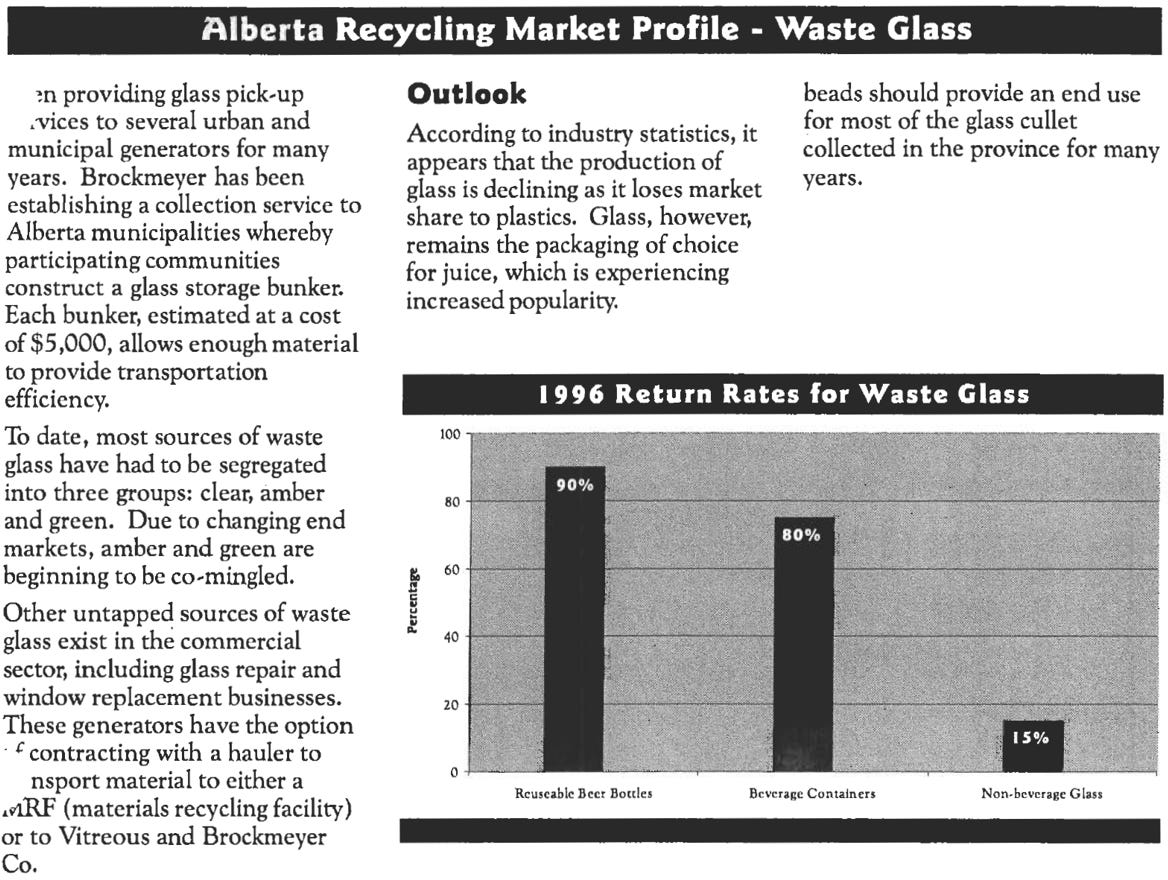

This snippet from the late 90s gives a sense of the history and consistency.

The new source

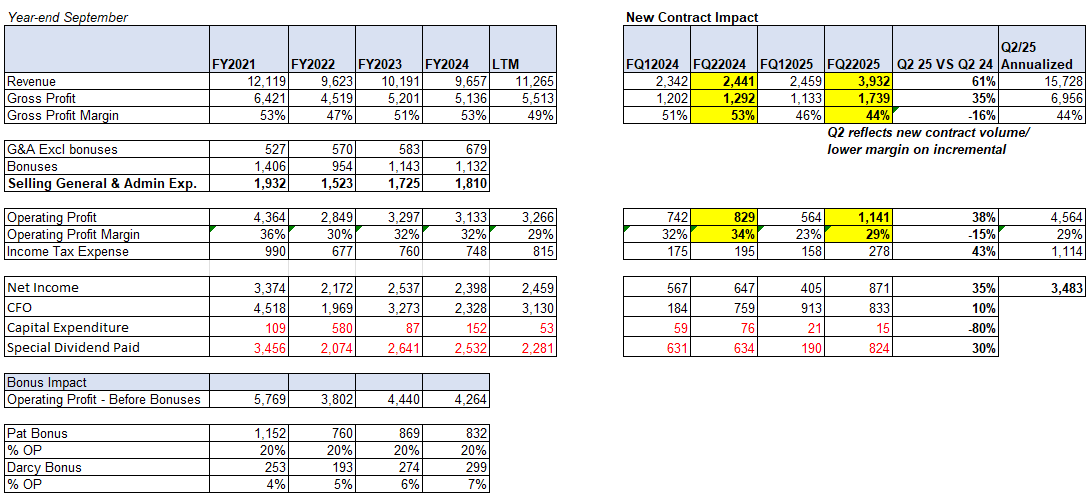

For a quiet business, seeing sales go up by 60% year-over-year does not happen often. The new source? One of their customers has found a glass source that they are getting Vitreous to process as part of a tolling agreement. Their customer is not in the business of crushing glass.

The level of business activity and revenue generated on a quarterly basis is highly dependent on the availability of raw glass for purchase and use in the Company’s Alberta based operation. During Q2 2025, the Company earned net income of $870,772 ($0.14 per share), a $465,399 increase compared to Q1 2025 during which there was the drop in sales volumes processed coinciding with a customer’s facility being idled for an extended period of time for maintenance. Q2 2025 net income was 34.6% or $223,645 higher compared Q2 2024 when the Company earned $647,127 ($0.10 per share) and which could be considered a quarter with a normal level of operations, excluding income earned from tolling. Sales during Q2 2025 increased by 59.9% to $3,932,091 compared to Q1 2025 and increased by 61.1% compared to the second quarter of 2024. Concurrently, cost of sales increased by 65.3% to $2,193,194 compared to Q1 2025 and increased 91.0% compared to the second quarter of 2024. Commencing in December 2024, one of the Company’s major customers requested Vitreous toll process glass not normally available to it at both a cost and a sales price per ton higher than all other Company processed waste glass. This temporary, uncommitted arrangement with the customer, which may extend until the end of calendar year 2025, has revenue and raw materials input costing which are higher than Vitreous’ historical revenue and cost structure. These additional volumes were not available during fiscal year 2024. Approximately 26.0% of Q2 2025 sales volumes were generated utilizing these higher priced materials inputs.

The issue is the contract is short-term in nature. The Company is tight-lipped about the details, but it appears to us that it is potentially a longer-term source of new glass so long as they continue to perform.

Compensation

The key founder of Vitreous is Pat Cashion going back to 1992.