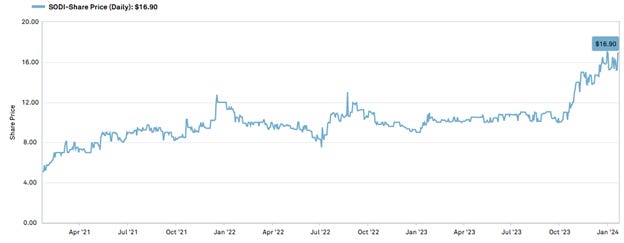

Solitron Devices, Inc. OTC:SODI Q3 Update

Here is the latest from Canadian Value Investors!

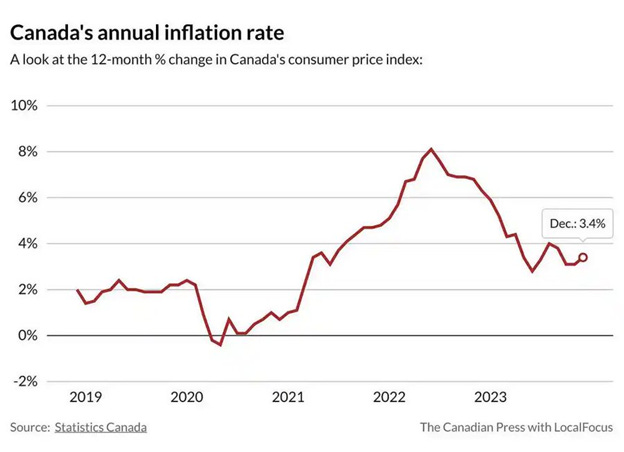

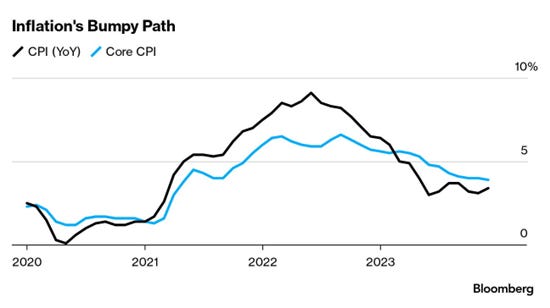

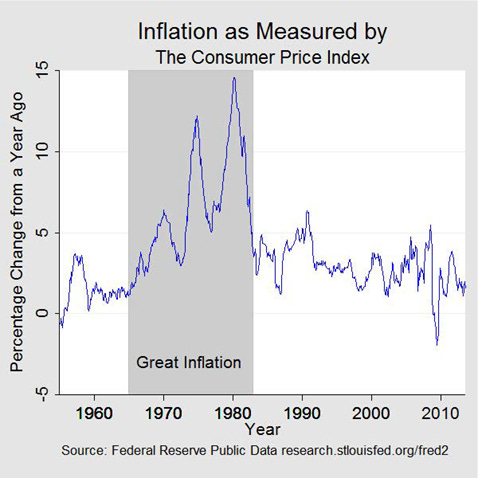

-CVI Soapbox - “Predicting” inflation

-Ideas from around the web

-Solitron Devices, Inc. OTC:SODI Q3 Update

“Predicting” inflation

We have been reading a lot of “when interest rates are cut in a month or two” type-analysis. Maybe rates will not get cut, or at least the pa. We would rather focus on companies that can float well in many different interest rate environments, rather than have our thesis even partially rely on something that even the “best” forecasters have such a bad track record of predicting - https://www.federalreservehistory.org/essays/great-inflation

Ideas from around the web

Disclosure: We have no positions in these at time of posting.

AerCap Holdings (AER)

“Imagine a stock trading below 8x fwd P/E. The CEO strategically sells company assets above book value and uses the proceeds to buy back shares below book value. They're on track to repurchase about 20% of their shares in 2023!”

Dada Nexus (DADA)

A Chinese last mile delivery service and on demand retail platform reported that about 500mn RMB ($70mn US) of revenue and costs were overstated for the first 3 reported quarters of 2023. Now trading below cash, and issue was not in core business, while key shareholder JD owns 50%.

Solitron Devices, Inc. OTC:SODI Q3 Update

Disclosure: We own this one.

We have been following Solitron since early 2022 and started purchasing shortly after the press released their acquisition of Micro Engineering, Inc.

https://microeng.com/

We have added the key posts from our www.canadianvalueinvestors.com archives to Substack for this update:

-First post in 2022 with full background - https://canadianvalueinvestors.substack.com/p/solitron-devices-inc-otcpksodi-reading

-June 2023 update - https://canadianvalueinvestors.substack.com/p/solitron-devices-inc-otcpksodi-is

There is a lot happening over at Solitron and thought it was worthwhile to do an update.

How are things going for Solitron?

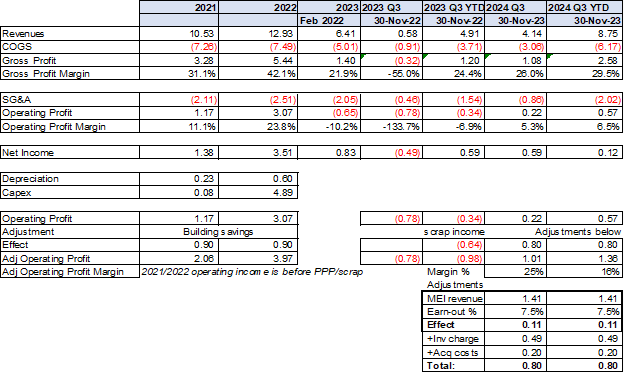

As a reminder, their core manufacturing business is power transistors and control modules primarily as a small but absolutely essential input into various weapons systems. It was historically run out of one leased facility, but in 2021 (under new leadership) they decided to find and purchase their own facility. They built up stock, closed down the old facility, and moved the equipment to the new facility. The move was done in the three months ending November 2022, or Q3 FY2023 (year-end is February to add to the confusion).

Note: If you are not familiar with Solitron, the full background post is essential.

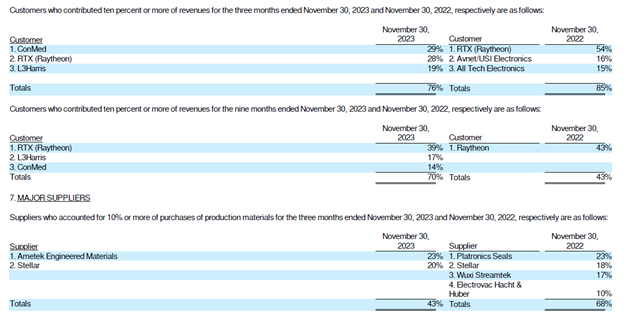

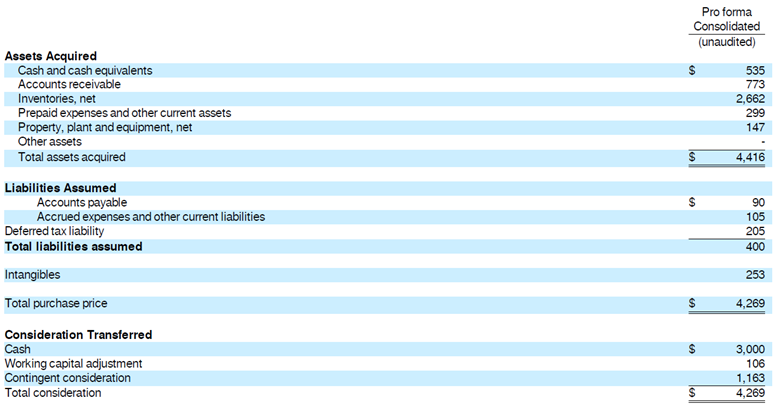

As we noted last summer, the Company stepped out of its core business into a somewhat related business, acquiring Micro Engineering, Inc. (see June 2023 update). As expected, more than half of MEI’s sales are to one customer, ConMed. You can see the before and after impact on customer concentration below:

Key question for the core defense business is the backlog, which seems healthy. Here are the notes year-over-year:

November 2022 note - Net bookings for the three months ended November 30, 2022 increased 68% to $2,257,000 versus $1,340,000 during the three months ended November 30, 2021. Backlog as of November 30, 2022 increased 101% to $6,430,000 as compared to a backlog of $3,197,000 as of November 30, 2021.

November 2023 Note - Net bookings for the three months ended November 30, 2023 increased 115% to $4,842,000 versus $2,257,000 during the three months ended November 30, 2022. Backlog as of November 30, 2023 increased 102% to $12,986,000 as compared to a backlog of $6,430,000 as of November 30, 2022.

The macro picture continues to get better for them (and unfortunately worse for global stability). For example, “the US said Patriot missile interceptors shot down a number of the missiles in Sunday’s attack [on a U.S. base in Iraq], which also involved rockets flying at lower altitudes, possibly in an attempt to overwhelm air defences.” The patriot system is one of the largest programs Solitron contributes to. https://www.thenationalnews.com/mena/iraq/2024/01/21/us-iraq-missile-attack-al-asad/

Sifting through the noise

With moving the facility, acquiring a second business, and gains and losses on marketable securities investments, the financial statements over the last few years are understandably noisy. Cedar Creek (the fund the CEO, Tim Eriksen, runs and now owns/controls over 15% of Solitron) provided additional context in their last letter:

https://www.eriksencapitalmgmt.com/investor-letters

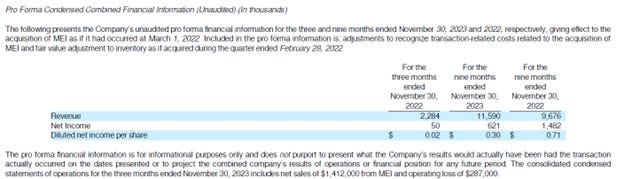

Subsequent to quarter end, Cedar Creek filed a Form 4 noting the fund purchased an additional 35,000 shares for $10.70 per share in a private transaction. Last week Solitron announced results for the fiscal third quarter ending November 30, 2023. Revenue was $4.1 million, and bookings were $4.8 million. Solitron reported earnings of $86,000 or $0.04 per share. There were a number of one-time items including a $494,000 impact to cost of goods sold due to acquisition related accounting requiring inventory to be marked at fair value on the acquisition date, $200,000 of acquisition related expenses, $21,000 of intangible amortization and $26,000 of non-cash interest expense. Reported operating income was $218,000, while “adjusted operating income” would have been over $930,000, or roughly $0.45 per share.

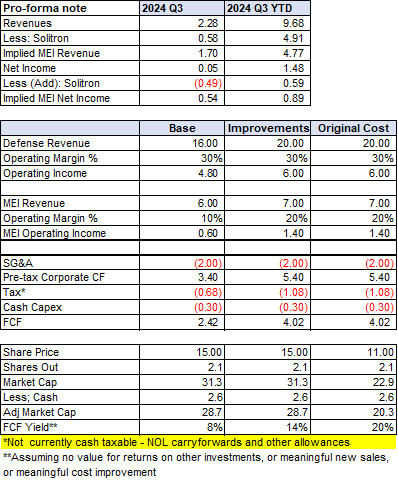

Assuming no value for returns on other investments, or meaningful new sales, or meaningful cost improvements as the current facility continues to ramp up, gets us to a base case. Other levers include surplus cash invested into future businesses or opportunistically in stocks (the latter providing roughly half a million of gains over the last two years), albeit surplus cash is now depleted with the cash acquisition of MEI ($2.6MM remaining vs $4.8MM last year-end).

It really comes down to 1) being comfortable with businesses that have an extremely concentrated customer base and are relatively opaque given their nature, and 2) whether you think Tim and Co will be good capital allocators. So far, so good.

Notes

Acquisition Accounting

Disclaimer - The content contained in this blog represents the opinions of contributors. You should assume contributors might have positions in the securities discussed and that this creates a conflict of interest regarding the objectivity of this blog. Statements in the blog are not guarantees of future performance whatsoever and are subject to certain risks, uncertainties and other factors. Information might also be completely out of date and may or may not be updated. No one guarantees the accuracy of any information provided and none of the information should be construed as investment advice under any circumstance. Frankly, no information here should be used for any purpose except for entertainment (and we hope you enjoy).