NFI Group Inc. TSX:NFI Q3 2025 Update - Is NFI a bus that’s going to keep breaking down?

A case study of the challenges of the green revolution.

Disclosure: We remain long.

We first wrote about NFI on February 9th. At the time we said:

Today we tell the tale of NFI, North America’s largest bus manufacturer. It has gone through several years of supply chain hell, only to emerge out of it into an unprecedented trade war with Trump. Why would you invest in a Canadian domiciled bus manufacturer in the middle of all of this?

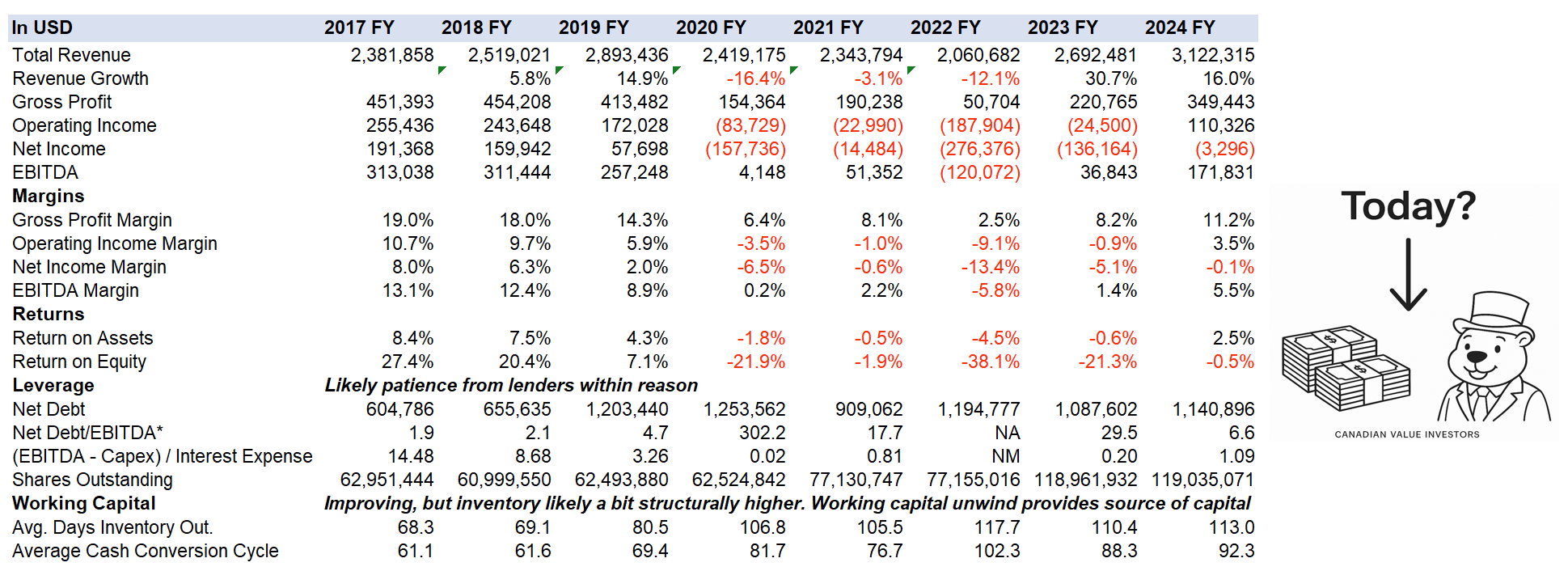

We think the market is missing the story. NFI is just turning the corner, returning to positive EBITDA, improved contracting and procurement processes, and a record $12 billion backlog, while many competitors have gone bankrupt or have exited the market. Now, North America is down to two key manufacturers of transit buses, with the other smaller one being at full capacity. And although NFI is headquartered in Canada, they have been producing buses for years that already comply with Buy America rules.

Based on the stock chart, our timing was quite good, and we do not expect to be able to repeat that. We reduced our position over the summer as we felt the stock got ahead of the underlying performance. Since then, two key things have happened. The first is, most notably, a major very expensive $230MM electric bus battery recall was press released in September causing the stock to pull back significantly (though still 30%+ above earlier this year). The second is the recently announced solution to the long running seating problem demonstrates that the competitive dynamics really have changed.

Is this a buying opportunity, or is this just a bad bus that cannot be fixed? We think the market has overreacted and is fatigued with the story. But, if “one-time” items keep happening, they need to considered recurring. We are not at that point, yet. Time for us to get back on that bus.

Here is our NFI Q3 2025 Update:

Bad batteries

Long-running seat issue solution found – Proof of the new competitive dynamics?

And tariffs

And debt

Outlook – “Never let a good crisis go to waste”

If you are not familiar with the story, we recommend you read our initial piece “Is this our bus?” and subsequent updates including their successful debt refinancing, full archives here - https://www.canadianvalueinvestors.com/t/nfi

Disclaimer - The content contained in this blog represents the opinions of contributors. You should assume contributors have positions in the securities discussed, whether long, short, or somewhere in between, and that this creates an obvious bias and conflict of interest regarding the objectivity of this blog. Statements in the blog are not guarantees of future performance whatsoever and are subject to certain risks, uncertain risks, and other factors. Information might also be completely out of date and may or may not be updated. In addition, no one guarantees the accuracy of any information provided and none of the information should be construed as investment advice or any other kind of advice under any circumstance, and the blog is a blog and not a registered investment advisor or broker in any jurisdiction. Frankly, no information here should be used for any purpose, except for entertainment (and we hope you enjoy).

Bad batteries

In September NFI announced some pretty bad news, a $230MM battery recall due to a few fires.

2025 North American Battery Recall

During the quarter, NFI initiated a voluntary recall with the National Highway Traffic Safety Administration and Transport Canada. The recall impacted approximately 700 battery-electric buses and coaches (primarily New Flyer buses) equipped with certain battery modules from a common supplier, XALT Energy, LLC (referred to as XALT). After issuing the recall, NFI deployed operational guidelines and software to limit the state of charge and speed of charging for the continued safe operation of the affected buses and coaches.

The Company has now determined that full battery replacement on these buses is required. NFI is finalizing its execution plan, with the replacement campaign expected to take approximately 18 to 24 months to complete, starting in the first half of 2026. In 2025 Q3, NFI recorded a warranty provision of $229.9 million, reflecting the estimated costs for full battery replacement on all the vehicles impacted by the recall and estimated future costs associated with supporting vehicles in service that have other older XALT batteries (collectively, the Battery Recall). NFI has executed a tentative term sheet with XALT regarding the ongoing battery recall and is working towards a definitive agreement concerning the associated costs.

Amounts accrued for the Battery Recall are based on management’s best estimates of the amounts that will ultimately be required to settle such items as of this writing. Adjustments to these figures may be made as changes in the cost estimates become known. These adjustments can have a favorable or unfavorable impact on NFI’s results.

Additionally, on October 28, 2025, XALT announced its decision to exit battery manufacturing, advising that it will wind down its

U.S. battery operations. XALT’s wind down does not change NFI’s expectation to finalize an agreement that meets the Company’s operational requirements and the needs of its customers.

NFI had previously taken proactive steps to move its primary battery supply for New Flyer battery-electric buses to a different supplier, who has been providing battery systems to NFI since 2023. This supplier is expected to provide batteries on new battery- electric buses in production and potentially the replacement of batteries on buses impacted by the recall.

This is expensive with a provision of ~US$328k per bus. However, the story is nuanced. NFI stopped using this battery provider, XALT, in 2023, and appears to have taken a very conservative charge while actual costs might be quite a bit lower. In addition, while a short-term headwind, we view this as a long-term tailwind. The ability to withstand major hiccups is absolutely essential with bus manufacturing, where contracts are large and demanding. Smaller incumbents and start ups just cannot withstand these types of issues, and many have failed because of them.

The XALT Recall

The battery is made by XALT. Here is the Transport Canada recall - https://recalls-rappels.canada.ca/en/alert-recall/transport-canada-recall-2025495-new-flyer

And the U.S. notice with better information. https://static.nhtsa.gov/odi/rcl/2025/RCLRPT-25V631-2095.pdf

The first event New Flyer received notice of was in August-2023 from a customer which reported smoke from a roof mounted battery pack. This battery pack was removed and ultimately sent to a third-party forensics team. Freudenberg and New Flyer worked cooperatively during the following months in an attempt to understand the issue.

Another report was received by New Flyer in June-2024. The battery pack from this bus was also sent to Freudenberg for analysis, and cooperation between the two companies continued.

6 more fires occurred between September-24 and July-2025.

Concurrent with these incidents, New Flyer learned of other battery-originated fires which were traced to different issues, leading to 24V625 (for our affiliate MCI only) and 25V566 (New Flyer). New Flyer’s Safety Committee met on 12-September-2025 and decided to conduct a safety recallfor the battery issue.

Interim remedy: Customers are recommended to avoid charging vehicles above a state of charge of 75%, remove buses from the charger once charged and park vehicles outdoors after charging. New Flyer will deploy a vehicle program update to limit the maximum State of Charge (SOC) to 75%, moderately reduce the charging current, and install enhanced post-charge battery monitoring and alert system. The post-charge battery monitoring and alert system will monitor the bus automatically for up to 2 hours after a charging session for any thermal anomalies. If any thermal anomalies are detected, the vehicle will automatically activate its hazard lights and audible buzzers to provide audible and visual alerts to anyone in proximity

It is a bit of an awkward situation, as XALT is winding down their operations. XALT is wholly owned by Freudenberg e-Power Systems (Freudenberg bought the remaining 49.9% in Jan-2023). https://www.freudenberg.com/en/company/press-media/news-detail/2023-01-09-freudenberg-acquires-remaining-ownership-interest-in-battery-manufacturer-xalt-energy-from-joint-venture-partner-mbp-investors However, the green-wave has hit a wall and XALT is just another victim. On Oct 28, 2025, Freudenberg announced it will wind down XALT’s Midland & Auburn Hills (MI) operations, citing weak heavy-duty EV demand.

The charge NFI is taking seems very conservative (and being applied to gross margin – “the Company would have reported a Gross Profit of $115.6 million, with gross margin of 13.1%, without the impact of the battery recall warranty provisions”). We note the parent of XALT is not going bankrupt, so there is potentially some recoverable amount. Conservatively, they have not booked any recovery. “NFI has executed a tentative term sheet with XALT regarding the ongoing battery recall and is working toward a definitive agreement concerning the associated costs. Although a non-binding term sheet has been executed with the supplier the outcome of these discussions remains uncertain. As such, no recoverable amount has been recognized in the financial statements at this time.” They expect XALT will provide the batteries before being wound down and will complete replacements over the next two years.

Long-running seat issue solution found – Proof of the new competitive dynamics in transit buses?