Berkshire Cash, Charlie Munger’s List, and Value Investing Event for Subscribers

Here’s the latest from Canadian Value Investors!

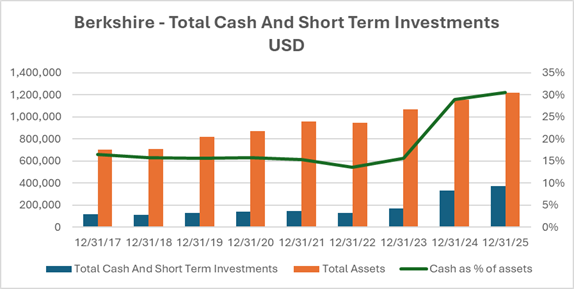

Berkshire Cash

Charlie Munger’s Standard Causes of Human Misjudgement

Calgary Value Investing Event Next Week

Disclosure: We own BRK (they’re Bs for the nosy)

The seed of Canadian Value Investors goes back to a Berkshire Hathaway AGM over a decade ago. We attended the Woodstock for Capitalists a few times, though we did not make a pilgrimage down this year.

Berkshire is going through a changing of the guard as we all know, and the cash pile continues to grow. Although part of it is just Berkshire getting bigger, the actual cash holdings as a percentage of assets is increasing now too. What a problem to have. We wish Greg Abel the best (even though he is from Edmonton). Jokes aside, Berkshire is on very stable ground and we believe it will continue to do well, just not as well as before.

With another Berkshire Hathaway AGM passing in early May, we are a little nostalgic and thinking about Charlie Munger, former right-hand man to Warren Buffett who passed away in 2023.

Charlie Munger’s Standard Causes of Human Misjudgment

We had the opportunity to see Charlie a few times at the Berkshire Hathaway AGM and also in California at the Daily Journal AGM. In fact, this blog was inspired by our first pilgrimage down to Omaha.

About once a year we sit down to listen to a talk he gave in 1995 called the Standard Causes of Human Misjudgement. We are all biased and the mind is easy to trick, which are big problems when it comes to investing. He created a concise list of biases to watch out for with entertaining stories to boot. To have even a chance of being a good investor, we think that being aware of these biases is essential. We miss you, Charlie.

Here is Charlie Munger’s Standard Causes of Human Misjudgment:

Under-recognition of the power of what psychologists call ‘reinforcement’

and economists call ‘incentives.’My second factor is simple psychological denial.

Incentive-cause bias, both in one’s own mind and that of ones trusted

adviser, where it creates what economists call ‘agency costs.’This is a superpower in error-causing psychological tendency: bias

from consistency and commitment tendency, including the tendency to avoid or

promptly resolve cognitive dissonance. Includes the self-confirmation tendency of

all conclusions, particularly expressed conclusions, and with a special persistence

for conclusions that are hard-won.Bias from Pavlovian association, misconstruing past correlation as a reliable

basis for decision-making.Bias from reciprocation tendency, including the tendency to act as other persons expect.

Now this is a lollapalooza, and Henry Kaufman wisely talked about this:

bias from over-influence by social proof -- that is, the conclusions of others,

particularly under conditions of natural uncertainty and stress.What made these economists love the efficient market

theory is the math was so elegant.Bias from contrast-caused distortions of sensation, perception and cognition.

Bias from over-influence by authority.

Bias from deprival super-reaction syndrome, including bias caused by

present or threatened scarcity including threatened removal of something almost

possessed but never possessed.Bias from envy/jealousy.

Bias from chemical dependency.

Bias from mis-gambling compulsion.

Bias from liking distortion, including the tendency to especially like oneself, one’s

own kind and one’s own idea structures, and the tendency to be especially

susceptible to being misled by someone liked. Disliking distortion, bias from that,

the reciprocal of liking distortion and the tendency not to learn appropriately

from someone disliked.Bias from the non-mathematical nature of the human brain in its natural state as it deal with probabilities employing crude heuristics, and is often misled by mere contrast, a tendency to over-weight conveniently available information and other psychologically misrouted thinking tendencies on this list.

Bias from over-influence by extra-vivid evidence.

Mental confusion caused by information not arrayed in the mind and theory structures, creating sound generalizations developed in response to the question “Why?” Also, mis-influence from information that apparently but not really answers the question “Why?” Also, failure to obtain deserved influence caused by not properly explaining why.

Other normal limitations of sensation, memory, cognition and knowledge.

Stress-induced mental changes, small and large, temporary and permanent.

Other common mental illnesses and declines, temporary and permanent, including the tendency to lose ability through disuse.

Development and organizational confusion from say-something syndrome.

[Paraphrasing] The above can be combined to greatly increase their power to change behavior, regarded by Charlie as the lollapalooza effect.

Calgary Value Investing Event Next Week